| City / Bank | Rate or Price | Key Detail |

|---|---|---|

| Bajaj Housing Finance | 7.25% p.a. onwards | Home loan interest rate |

| Bank of India | 7.10% – 10.25% p.a. | Home loan interest rate range |

| Canara Bank | 7.15% – 10.00% p.a. | Home loan interest rate range |

| Bank of India | 7.10% p.a. onwards; 10.65% p.a. | Floating and fixed rates; processing fee 0.25% of loan amount |

| HDFC Bank | 7.75%* p.a. onwards | EMIs starting from ₹716 per lac |

| Standard Home Loan | 8.50% – 9.40%; 8.50% – 9.55% | Loan amount up to ₹35 lakh |

Data sourced from top search results. Verify before making decisions.

Buying a home can feel exciting until you see how much interest you may pay over 15, 20, or 25 years. Even a small difference of 0.25% in your home loan rate can change your EMI and total cost by lakhs of rupees.

The good news is that home loan rates in India are still competitive, with many lenders starting around the 7.10% to 7.75% per year range for eligible borrowers. But the lowest rate is not given to everyone, so you need to know what banks actually check.

What Home Loan Rates in India Look Like Right Now

Most banks and housing finance companies offer home loans on a floating interest rate. This means your rate can move up or down when the lending benchmark changes.

Some lenders also offer fixed-rate options, but these are often higher than floating rates. For example, a bank may offer floating rates starting near 7.10% p.a., while its fixed rate can be much higher.

Sample Rate Range Across Popular Lenders

| Lender Type / Example | Indicative Home Loan Rate | What to Check |

|---|---|---|

| Public sector banks | About 7.10% to 10.25% p.a. | Credit score, salary account, processing fee |

| Private banks | About 7.60% to 11% p.a. | EMI offer, top-up loan, service speed |

| Housing finance companies | About 7.25% p.a. onwards | Eligibility, property approval, foreclosure rules |

These are only broad market ranges. Your final rate can be different based on your profile and the property you buy.

Why Two People May Get Different Rates from the Same Bank

Many borrowers think one bank has one home loan rate for everyone. That is not true. Banks use risk-based pricing, which means safer borrowers often get better rates.

1. Your Credit Score Matters

A high credit score tells the bank that you repay loans on time. If your score is above 750, you may get a lower rate than someone with a weaker score.

Before you apply, check your credit report and fix errors. A clean repayment record can help you save money for many years.

2. Your Income and Job Stability Count

Banks like steady income. Salaried borrowers with stable jobs often get quick approvals, while self-employed borrowers may need to show stronger documents.

If your income is irregular, keep your income tax returns, bank statements, and business records ready. This can improve your chances of getting a fair rate.

3. Loan Amount and Property Type Also Affect Pricing

A ready-to-move flat in an approved project may be easier to finance than a property with unclear papers. Banks also check the builder, location, title, and legal documents.

If you are still deciding whether to buy now, this guide on 9 smart checks before you buy a flat in May 2026 can help you compare rates, rent, and real costs.

Floating vs Fixed Home Loan Rate: Which Is Better?

A floating rate changes with market conditions. It usually starts lower than a fixed rate and is common in India.

A fixed rate gives more certainty, but it may cost more. Also, some “fixed” loans are fixed only for a few years and then change to floating.

Simple Rule to Choose

If you want a lower starting EMI and can handle small changes, floating can work well. If you hate any EMI change and are ready to pay extra for peace of mind, fixed may suit you.

Do Not Compare Only the Interest Rate

The lowest rate is attractive, but it is not the full story. A loan with a low rate but high charges may not be the cheapest.

Check These Costs Before Signing

- Processing fee: Some banks charge a percentage of the loan amount, with minimum and maximum limits.

- Legal and valuation charges: These may be separate from the processing fee.

- Insurance cost: Loan protection insurance may be offered, but understand if it is optional.

- Prepayment rules: Floating-rate home loans usually have friendly prepayment terms for individuals, but always confirm.

- Reset frequency: Ask how often your floating rate can change.

For a deeper look at rate movements and what borrowers should watch, read 7 key things to know about home loan interest rates in India in May 2026.

7 Smart Moves to Get a Better Home Loan Rate

1. Compare at Least 4 Lenders

Check public banks, private banks, and housing finance companies. Do not stop at the first offer, even if it is from your salary bank.

2. Ask for the Rate Based on Your Credit Score

Do not ask only, “What is your home loan rate?” Ask, “What rate can I get with my credit score and income?” This gives you a more useful answer.

3. Keep a Bigger Down Payment Ready

A higher down payment lowers the bank’s risk. It can also reduce your EMI and total interest burden.

4. Avoid New Loans Before Applying

Do not take a personal loan, car loan, or large credit card EMI just before applying. It can reduce your home loan eligibility.

5. Negotiate the Processing Fee

Many borrowers negotiate only the interest rate. But processing fees can also be reduced during special offers or festive campaigns.

6. Use a Co-Applicant if It Helps

Adding a working spouse can improve eligibility. It may also help you buy a better property without stretching your finances too much.

7. Test the EMI Before You Commit

Do not take the maximum loan just because the bank approves it. Your EMI should leave room for school fees, medical costs, savings, and emergencies.

If you are unsure whether buying is better than renting, use these 5 money tests before you stop renting in May 2026 before making the move.

FAQ: Home Loan Rates in India

What is the current home loan rate in India?

Home loan rates in India currently start around 7.10% to 7.75% p.a. for many lenders, but the actual rate depends on your credit score, income, property, loan amount, and bank policy.

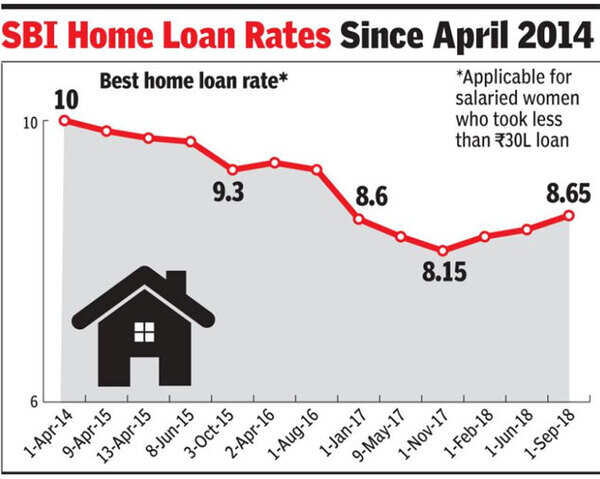

What are SBI home loan rates in India?

SBI home loan rates change from time to time and depend on the borrower’s profile. You should check the latest SBI rate card and compare it with other public and private banks before applying.

Which bank gives the best home loan rate?

There is no single best bank for everyone. Public sector banks may offer strong rates, private banks may offer faster service, and housing finance companies may be more flexible for some borrowers.

Is the Bank of India home loan interest rate low?

Bank of India has been seen offering floating home loan rates from around 7.10% p.a. onwards, subject to eligibility. It may also charge a processing fee, so compare the total cost before choosing.

Is there a government home loan interest rate?

The government does not usually set one common home loan rate for all buyers. However, eligible borrowers may benefit from housing schemes or subsidies when available, so check current scheme rules before applying.

Final Recommendation

Choose a home loan only after comparing the interest rate, processing fee, EMI, prepayment rules, and property approval process. If your credit score is strong and your income is stable, push the bank for a better rate instead of accepting the first offer.

The best move is simple: shortlist 3 to 4 lenders, get written offers, calculate the full cost, and pick the loan that stays affordable even if rates rise later.

“The best move is simple: shortlist 3 to 4 lenders, get written offers, calculate the full cost, and pick the loan that stays affordable even if rates rise later.”

*Affiliate link — we may earn a small commission at no extra cost to you.

Millennial writer covering everyday money struggles, price hikes, and life in India through a Gen-Z lens. Writes the way real people talk — no jargon, just facts.