| City / Bank | Rate or Price | Key Detail |

|---|---|---|

| HDFC Bank | 7.75% p.a. onwards | EMIs starting from ₹716 per lac |

| Home Loan Interest Rates | 7.10% p.a. onwards | Processing fee starting from 0.25% of the loan |

| EMI Calculation Example | 8.40% | EMI ₹73,228; principal amount ₹85,00,000; interest amount ₹90,74,692 |

| Bajaj Housing Finance | 7.25% p.a. onwards | Listed under current home loan interest rates |

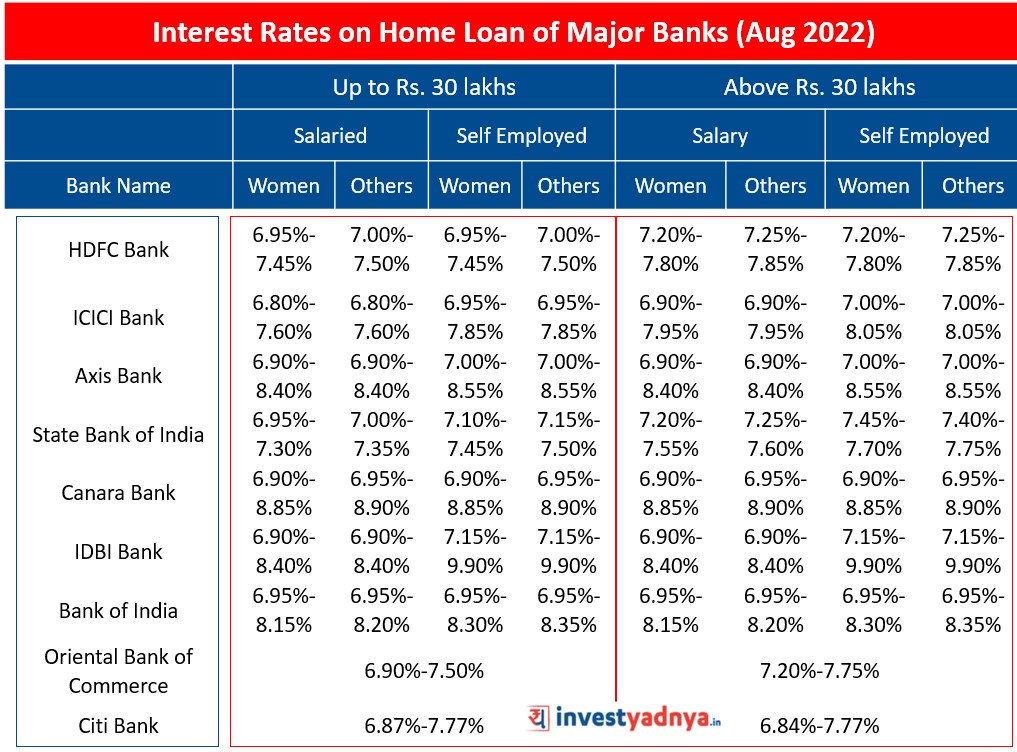

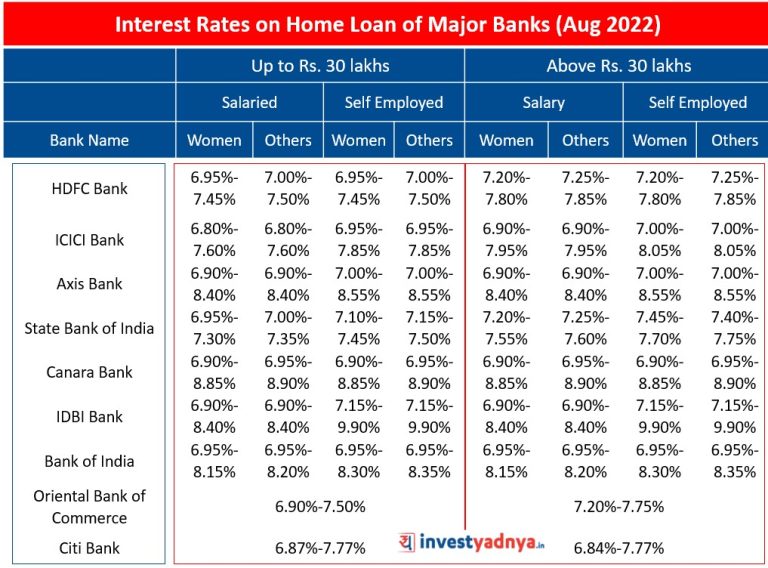

| Bank of India | 7.10% – 10.25% p.a. | Listed under current home loan interest rates |

| Canara Bank | 7.15% – 10.00% p.a. | Listed under current home loan interest rates |

Data sourced from top search results. Verify before making decisions.

A small difference in your home loan interest rate can cost you lakhs over 15 to 25 years. Many buyers only look at the EMI, but the real cost is hidden in the total interest you pay.

If you are planning to buy a house in India, do not rush just because one bank shows a low starting rate. The best loan is not always the one with the lowest number in the ad.

Why India Home Loan Interest Rate Matters So Much

A home loan is usually the biggest loan most families take. Even a 0.25% difference in rate can change your monthly EMI and long-term interest cost.

For example, on a ₹50 lakh loan for 20 years, a slightly higher rate may look small every month. But over the full loan period, it can mean paying a few lakhs more.

Do Not Trust Only the “Starting From” Rate

Banks and housing finance companies often show rates like starting from 7.10% p.a. or starting from 7.75% p.a. These are usually for borrowers with strong credit scores, stable income, and low-risk profiles.

Your actual offer may be higher. That is why you should ask for a written loan quote before making a decision.

Key Home Loan Interest Rate Data to Know

Rates change often, so use the table below as a guide, not a final quote. Always check directly with the lender before applying.

| Item | Typical Detail | Why It Matters |

|---|---|---|

| Starting interest rate | About 7.10% to 7.75% p.a. | Your final rate may be higher based on your profile. |

| Processing fee | Often starts near 0.25% of loan amount | This adds to your upfront cost. |

| EMI example | Some lenders show EMIs from around ₹716 per lakh | Actual EMI changes with rate and tenure. |

| EMI calculator | Available on most bank websites | Helps compare monthly payments quickly. |

How Banks Decide Your Home Loan Rate

1. Your Credit Score

A high credit score can help you get a better rate. Many banks prefer borrowers with a score above 750.

If your score is low, you may still get a loan, but the rate can be higher. Before applying, check your credit report and fix errors if any.

2. Your Income and Job Type

Banks like stable income. Salaried employees in well-known companies may get easier approval than people with irregular income.

Self-employed borrowers can also get good rates, but they may need to show income tax returns, bank statements, and business proof.

3. Loan Amount and Down Payment

If you borrow less compared to the property value, the bank sees less risk. A larger down payment can sometimes help you get better terms.

Try to avoid taking the maximum loan just because the bank approves it. A smaller loan means lower EMI pressure.

4. Fixed vs Floating Rate

Most Indian home loans are linked to floating rates. This means your EMI or loan tenure can change when benchmark rates move.

A fixed rate gives more peace of mind, but it may start higher. Check reset clauses carefully before signing.

How to Use a Home Loan EMI Calculator the Right Way

A home loan interest rate calculator or EMI calculator helps you estimate your monthly payment. You only need three details: loan amount, interest rate, and tenure.

The standard EMI formula is based on principal, monthly interest rate, and number of months. But you do not need to calculate it by hand because bank calculators do it instantly.

Sample EMI for a ₹20 Lakh Home Loan

Here is an easy example for a ₹20 lakh loan for 20 years:

| Interest Rate | Approx. Monthly EMI |

|---|---|

| 7.5% p.a. | ₹16,100 |

| 8.0% p.a. | ₹16,700 |

| 8.5% p.a. | ₹17,350 |

| 9.0% p.a. | ₹18,000 |

These numbers are only estimates. Your final EMI may change due to insurance, fees, rate type, and bank rules.

9 Smart Checks Before Choosing a Home Loan

1. Compare at Least 3 Lenders

Do not stop at your salary bank. Compare public banks, private banks, and housing finance companies.

2. Ask for the Final Rate, Not Just the Lowest Rate

Tell the bank your income, credit score, property value, and loan amount. Then ask for the exact rate they can offer you.

3. Check the Processing Fee

A lower rate with a high processing fee may not always be better. Compare the full cost, not just the EMI.

4. Look at Prepayment Rules

If you plan to make extra payments, check if there are charges. Many floating-rate loans for individuals have friendly prepayment rules, but confirm first.

5. Test EMI at a Higher Rate

If your rate is floating, your EMI can rise later. Check if you can still pay comfortably if the rate goes up by 1%.

6. Keep EMI Below a Safe Limit

Try to keep all loan EMIs under 40% of your monthly take-home pay. This gives space for bills, school fees, medical needs, and savings.

7. Read the Reset Clause

Some loans change rates based on repo-linked or external benchmark systems. Ask how often your rate can change.

8. Do Not Ignore Insurance Costs

Some lenders may suggest loan insurance. It can be useful, but check the premium and whether it is added to your loan.

9. Think About Rent vs Buy

Before taking a large loan, check whether buying now truly fits your budget. This guide on 5 Money Tests Before You Stop Renting in May 2026 can help you make a clearer choice.

When Is a Home Loan Rate Actually Good?

A good rate is not just the lowest number online. It is a rate that comes with fair fees, clear terms, and an EMI you can pay without stress.

If you are tracking current market movement, this article on 7 Key Things to Know About Home Loan Interest Rates in India in May 2026 explains important rate trends in simple terms.

FAQ

What is the current India home loan interest rate?

Many lenders advertise starting rates around 7.10% to 7.75% p.a. However, your actual rate depends on your credit score, income, loan amount, and property details.

Which bank has the lowest home loan interest rate in India?

The lowest rate changes often. SBI, HDFC Bank, ICICI Bank, Axis Bank, Bank of Baroda, and other lenders may offer competitive rates at different times.

What is the EMI for a ₹20 lakh home loan?

For a ₹20 lakh loan over 20 years, the EMI may be around ₹16,100 to ₹18,000 if the rate is between 7.5% and 9%. Use an EMI calculator for exact numbers.

Is SBI home loan interest rate better than private banks?

SBI can be competitive, especially for borrowers with strong credit profiles. But private banks may offer faster processing or special deals, so compare both.

Should I choose a longer tenure to reduce EMI?

A longer tenure lowers your EMI but increases total interest. Choose a tenure that keeps EMI comfortable, then prepay when you have extra money.

Final Recommendation

Choose a home loan only after comparing the interest rate, EMI, processing fee, prepayment rules, and total interest cost. If the EMI fits your budget even after a possible rate rise, and the loan terms are clear, then it is a smart deal.

Do not chase the lowest advertised rate blindly. Pick the loan that protects your monthly cash flow and helps you own your home without long-term money stress.

*Affiliate link — we may earn a small commission at no extra cost to you.

“*Affiliate link — we may earn a small commission at no extra cost to you.”

Personal finance writer with 6+ years covering Indian markets, home loans, and investment strategies. Based in Mumbai. Obsessed with helping middle-class Indians build real wealth.