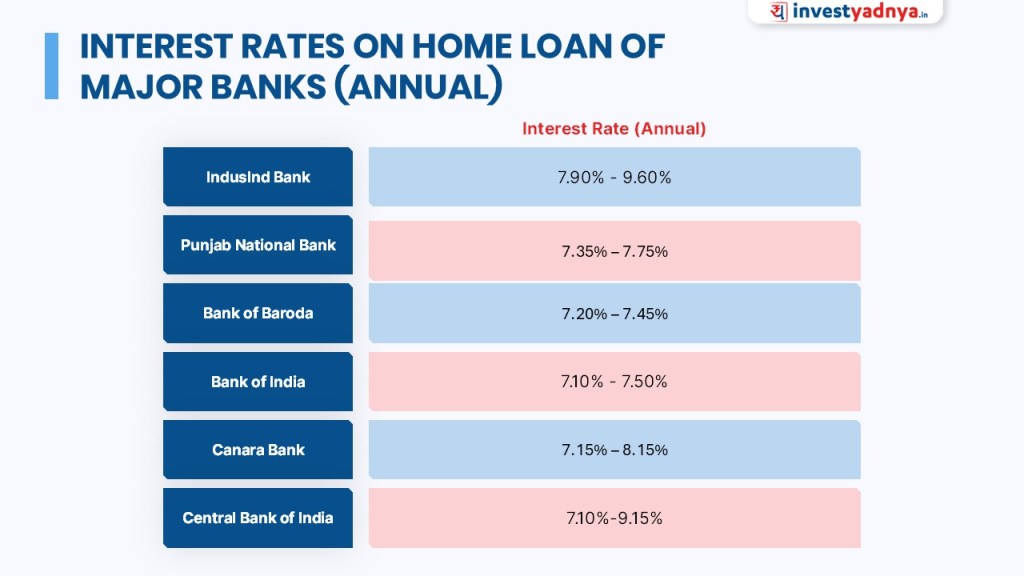

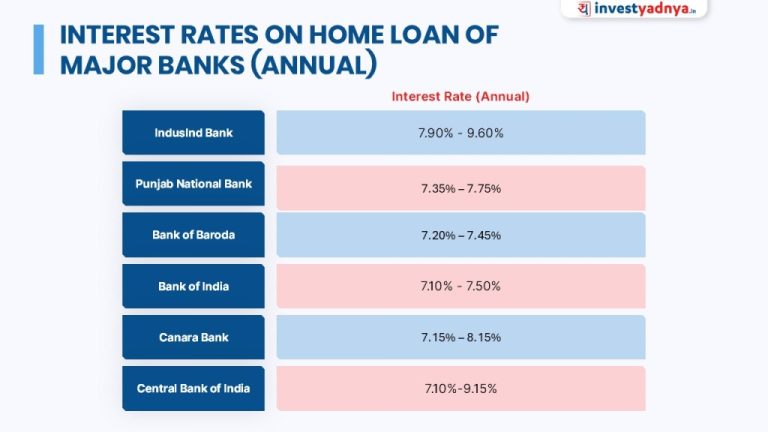

| City / Bank | Rate or Price | Key Detail |

|---|---|---|

| India property market | Property prices steadily increasing | Financially prepared buyers may benefit more from buying now |

| Unspecified home loan provider | Starting from 7.25%* p.a. | Attractive interest rates for easy home loan |

| Home Loans | Now from 7.85% p.a. | Mentioned with home loan balance transfer |

| India home loan rates 2026 | Stable or decline marginally | Most economists expect rates to remain stable or decline marginally |

Data sourced from top search results. Verify before making decisions.

A small change in home loan rates can look harmless, but on a 20-year loan it can add lakhs to your total cost. At the same time, waiting for a cheaper rate may not help if the flat price rises faster than the rate falls.

That is the real problem for buyers in May 2026: should you buy the house now or wait for lower home loan rates? The answer depends less on headlines and more on your cash flow, job safety, and the price of the property you want.

Home Loan Rates in India in May 2026: What Buyers Should Know

In May 2026, home loan rates in India are still attractive compared with many past years. Some lenders are advertising rates starting around 7.25% per year, while many common offers are closer to 7.85% per year or higher, depending on your profile.

Your actual rate can change based on your credit score, income, loan amount, property type, and whether you are salaried or self-employed. Women borrowers may also get a small rate benefit from some banks or housing finance companies.

Will home loan interest rates go down in 2026?

Most experts expect rates to stay mostly stable or move down only a little in 2026. That means waiting for a big fall may not be a strong plan.

If a rate falls by 0.25%, your EMI will reduce, but not always enough to beat a rise in property price. For many buyers, the bigger risk is not the rate. It is buying a costlier home six months later.

The Big Question: Buy Now or Wait?

Do not decide only by looking at the lowest rate on a bank website. The better question is: can you afford the home even if the rate goes up slightly?

If the answer is yes, buying now can give you price certainty. If the answer is no, waiting and saving more money is safer.

When buying now makes sense

You can consider buying in May 2026 if you have at least 15% to 25% of the property price ready as your own money. You should also have a separate emergency fund for six months of expenses.

Your EMI should ideally stay below 35% to 40% of your monthly take-home income. If your rent is already high and you plan to live in the same city for many years, buying may be a smart move.

When waiting is better

Wait if your job is not stable, your credit score is weak, or you are borrowing money for the down payment. Also wait if the builder has unclear approvals or the flat price feels stretched.

A home should not make your life stressful every month. Before you move from rent to EMI, check your numbers using 5 Money Tests Before You Stop Renting in May 2026.

Key Data: Rate, Price, and EMI Impact

| Factor | May 2026 Buyer View | What It Means |

|---|---|---|

| Starting home loan rates | Around 7.25% p.a. for select borrowers | Best rates need strong credit and income |

| Common rate range | Often around 7.85% p.a. or more | Compare banks before applying |

| Rate outlook | Stable or small decline expected | Do not wait only for a big rate cut |

| Property prices | Rising in many areas | Delay may increase total cost |

6 Clear Signs You Should Buy in May 2026

1. Your EMI is comfortable, not painful

A home loan should fit your life. If the EMI leaves you with enough money for food, school fees, travel, insurance, and savings, you are in a better position to buy.

Do not take the highest loan amount the bank offers. Take the amount you can repay without fear.

2. You have a strong credit score

A good credit score can help you get a lower interest rate. Even a small rate difference matters when the loan runs for 15 to 25 years.

Before applying, clear overdue payments and reduce credit card balances. This can improve your chance of getting a better offer.

3. The property is for long-term use

Buying makes more sense if you will live in the home for at least seven to ten years. Short-term buying can be costly because of stamp duty, registration, brokerage, moving costs, and loan charges.

If you may shift cities soon, renting may still be better.

4. You have compared rent with EMI

In some cities, rent is rising fast. If your rent is already close to a possible EMI, buying can be worth checking seriously.

But remember, EMI is not the only cost. You must add maintenance, property tax, parking, interiors, and repair costs. For a deeper checklist, use 9 Smart Checks Before You Buy a Flat in May 2026: Rates, Rent and Real Costs.

5. The builder and papers are clean

A cheap flat can become expensive if legal papers are weak. Check RERA registration, land title, building approvals, possession date, and past delivery record.

If you are buying a resale home, check loan closure papers, society dues, property tax receipts, and sale deed history.

6. You are not buying only because of fear

Do not buy because relatives say prices will double. Also do not wait forever because someone says rates will crash.

Buy when the numbers work. A calm decision is better than a rushed one.

Step-by-Step Plan Before You Apply for a Home Loan

Step 1: Check your real budget

Start with your monthly income and fixed expenses. Then decide the EMI you can pay safely.

Keep money aside for stamp duty, registration, furniture, shifting, and emergency needs. These costs can surprise first-time buyers.

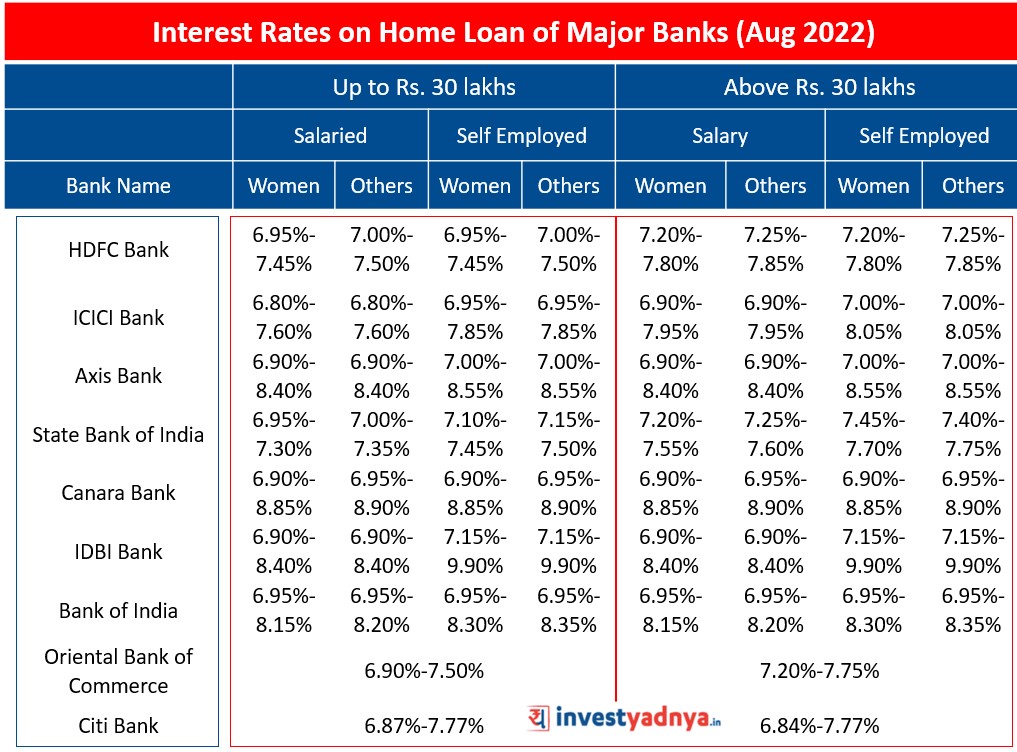

Step 2: Compare at least 4 lenders

Check SBI home loan rates, private bank rates, housing finance companies, and offers for women borrowers if applicable. Do not look only at the interest rate.

Compare processing fees, legal charges, prepayment rules, insurance pressure, and reset periods for floating loans.

Step 3: Use a home loan interest rate calculator

A calculator helps you see EMI, total interest, and loan tenure. Test the EMI at today’s rate and also at 0.50% higher.

If the higher EMI still feels safe, your plan is stronger.

Step 4: Keep balance transfer in mind

If you already have a home loan at a higher rate, May 2026 may be a good time to check a balance transfer. But do the math first.

Transfer only if the savings are higher than the fees and paperwork cost.

FAQs

What are the best home loan rates in India in May 2026?

Some lenders are showing starting rates near 7.25% per year for selected borrowers. Your final rate depends on credit score, income, loan size, employer type, and property details.

Are SBI home loan interest rates the lowest?

SBI is often competitive, but it may not always be the lowest for every borrower. Compare SBI with other public banks, private banks, and housing finance companies before choosing.

Do women get lower home loan interest rates?

Some lenders offer a small discount to female borrowers or co-borrowers. The benefit may be small, but over a long loan period it can still save money.

Should I choose fixed or floating home loan rates?

Floating rates can move up or down with the market. Fixed rates give more certainty, but may start higher or come with conditions. Read the loan terms carefully.

Is it better to buy a house now or wait until rates fall?

If your finances are ready and the property is fairly priced, buy now. If your EMI is too high or your savings are weak, wait and build a safer base first.

Final Recommendation

Buy a home in May 2026 if your EMI is affordable, your down payment is ready, and you plan to stay long term. Waiting only for a big rate cut is not a strong strategy because rates may fall only a little while property prices may keep rising.

If your budget is tight, do not force the purchase. Save more, improve your credit score, and return to the market with stronger numbers.

“If your budget is tight, do not force the purchase.”

*Affiliate link — we may earn a small commission at no extra cost to you.

Tech writer and gadget reviewer based in Delhi. Covers AI tools, global tech trends, and consumer electronics. Reviews products thoroughly before recommending them.