Your rent may feel “wasted” every month, but a home loan EMI can quietly eat more of your salary than you expect. In May 2026, many Indian families are asking the same question: should we buy now, or keep renting and wait?

The tricky part is that both choices can be smart. The right answer depends less on headlines and more on your cash flow, job stability, city, and how long you plan to stay.

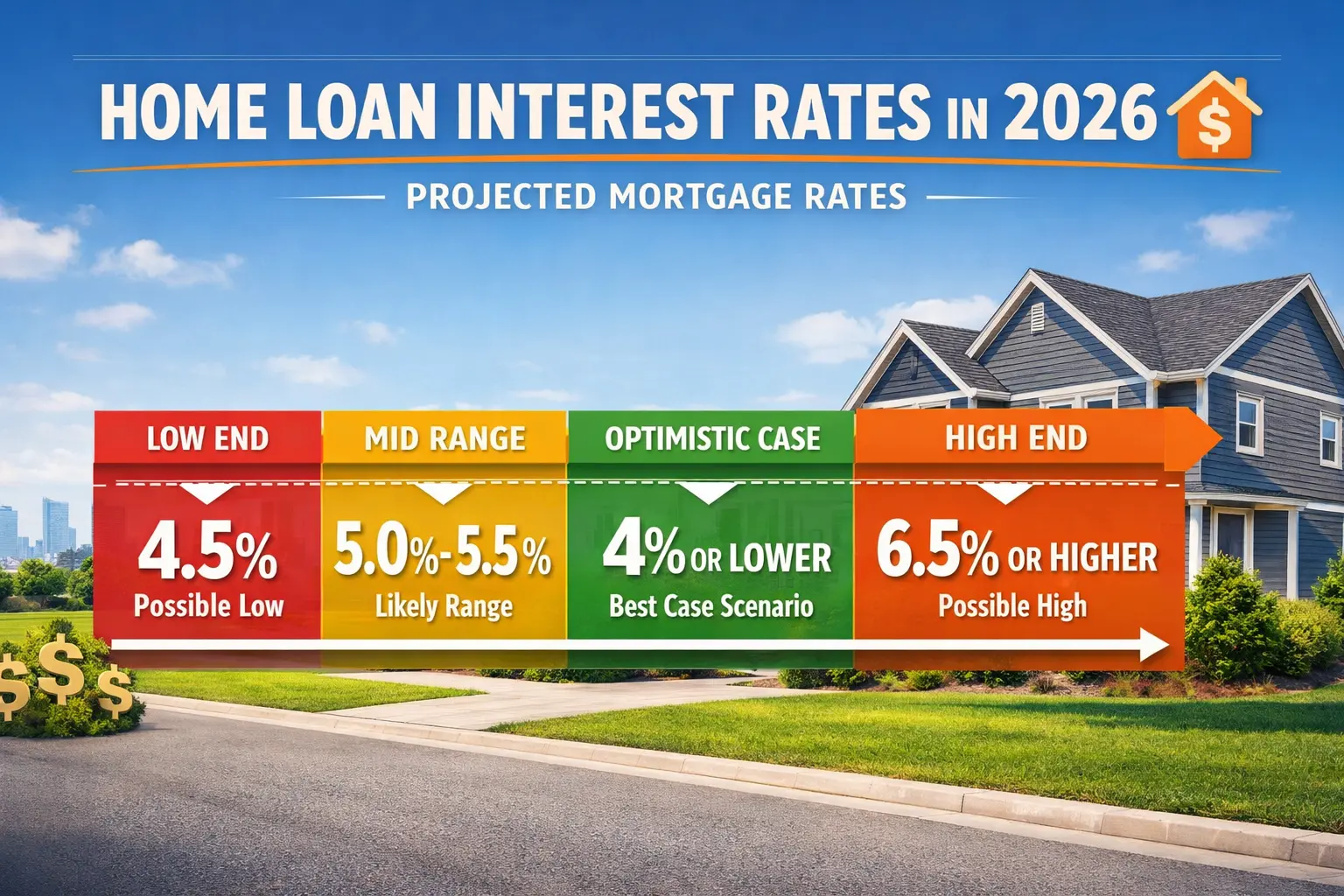

Why May 2026 Feels Like a Confusing Time to Buy

Home loan rates in India are expected to be more stable than the sharp rate-change years before, but that does not mean loans are cheap for everyone. Banks still price loans based on your credit score, income, loan amount, property type, and risk profile.

At the same time, property prices in many cities remain high. Even if interest rates fall a little, the total cost of buying may still be heavy because stamp duty, registration, brokerage, maintenance, parking, and interiors add up fast.

The Big Trap: Comparing Rent With EMI Only

Many buyers say, “My rent is ₹30,000 and EMI is ₹45,000, so buying is better.” This is too simple. A real comparison should include down payment, lost investment returns, tax benefits, maintenance, property tax, and resale risk.

If you want a deeper checklist before making the jump, this guide on 5 Money Tests Before You Stop Renting in May 2026 can help you check your numbers in a practical way.

Buy or Rent in May 2026: Key Money Table

| Factor | Buying a Home | Renting |

|---|---|---|

| Monthly Cost | EMI is usually higher than rent in big cities | Lower monthly outflow in many locations |

| Flexibility | Harder to move for job or family needs | Easy to shift cities or upgrade/downgrade |

| Long-Term Value | Can build equity if you stay long enough | No ownership, but savings can be invested |

| Risk | Interest rate, builder delay, resale, and maintenance risk | Rent hikes and landlord issues |

| Best For | Stable income, long stay, strong savings | Career changes, uncertain city, lower savings |

7 Hard Signs You Are Ready to Buy

1. Your EMI Is Under Control

A safe rule is to keep total EMIs below 35% to 40% of your monthly take-home income. If your home loan EMI alone takes half your salary, the house may become a burden instead of a dream.

2. You Have a Real Down Payment

Do not depend on personal loans or credit cards for the down payment. You should ideally have enough savings for the down payment plus stamp duty, registration, shifting, basic furniture, and emergency needs.

3. You Will Stay for 7 to 10 Years

Buying works better when you stay long enough for the property to grow in value and for loan costs to balance out. If you may move cities in two or three years, renting may be smarter.

4. Your Job and Income Are Stable

A home loan is a long promise. If your income is irregular, your industry is unstable, or you are planning a career break, wait until your cash flow is stronger.

5. The Property Is Not Overpriced

Do not buy only because a broker says prices will rise soon. Compare similar homes in the area, check rental yield, builder record, legal papers, and future infrastructure plans.

6. You Are Buying for Use, Not FOMO

Fear of missing out is a bad reason to take a 20-year loan. Buy because the home fits your life, budget, commute, family needs, and long-term plan.

7. You Have Checked the Full Cost

The flat price is not the final price. Before booking, go through 9 Smart Checks Before You Buy a Flat in May 2026: Rates, Rent and Real Costs so you do not miss hidden expenses.

When Renting Is the Better Choice

You Are Still Building Savings

If buying will empty your bank account, keep renting. A house without emergency savings can create panic during job loss, illness, or family needs.

You Want Career Freedom

Renting gives you freedom to move closer to work, change cities, or take a better job. This is useful for young professionals, newly married couples, and people in fast-changing industries.

Your Rent Is Much Lower Than EMI

In many Indian metros, rent is far lower than the EMI for the same home. If you invest the difference wisely, renting can create wealth too.

Step-by-Step Guide Before You Decide

Step 1: Calculate the Real EMI

Check home loan offers from at least three lenders. Compare interest rate, processing fee, insurance, prepayment rules, and whether the loan is floating or fixed.

Step 2: Add All Extra Costs

Add stamp duty, registration, brokerage, legal fee, parking, interiors, maintenance deposit, GST if applicable, and moving costs. This gives you the real buying cost.

Step 3: Compare With Renting

Compare your yearly rent with your yearly EMI and extra ownership costs. Also compare what your down payment could earn if invested instead.

Step 4: Stress Test Your Budget

Ask yourself: can I pay the EMI if rates rise, bonus stops, or one income pauses? If the answer is no, wait and build more savings.

Step 5: Check the Property Like an Investor

Even if you plan to live there, think like an investor. Check location demand, metro or road access, water supply, builder quality, society charges, and resale chances.

FAQ

Will home loan interest rates go down in 2026 in India?

They may soften if inflation stays under control and the RBI supports lower rates. But no one can promise a clear fall, so buy only if the EMI is affordable at today’s rate.

Will housing loan interest reduce in 2026?

Some borrowers may get better offers if their credit score is strong and banks compete for good customers. Existing floating-rate borrowers may also benefit if benchmark rates move lower.

Will property rates go down in 2026?

Some overheated pockets may see slower growth or small corrections. But good locations with strong demand may not become much cheaper, especially in major job markets.

Is it better to buy a flat or keep renting in 2026?

Buy if you have stable income, plan to stay long term, and can manage the full cost. Rent if you need flexibility, have low savings, or your EMI will stretch your budget.

Should I wait for lower home loan rates?

Waiting only for lower rates can be risky because property prices may move up. A better plan is to wait until your finances are ready, not just until rates look attractive.

Final Recommendation

Buy in May 2026 if the home is for long-term use, the EMI is comfortable, and you still have emergency savings after paying the down payment. This is the right move for families with stable jobs, clear location plans, and a 7 to 10 year holding period.

Keep renting if buying will empty your savings, force a very high EMI, or lock you into a city you may leave. Renting is not failure; it is a smart financial choice when it protects your freedom and helps you build a stronger base for a better purchase later.

*Affiliate link — we may earn a small commission at no extra cost to you.

“*Affiliate link — we may earn a small commission at no extra cost to you.”

Bilingual content writer covering fintech, credit cards, and personal finance for readers in India, Brazil, and beyond. Believes financial literacy has no borders.