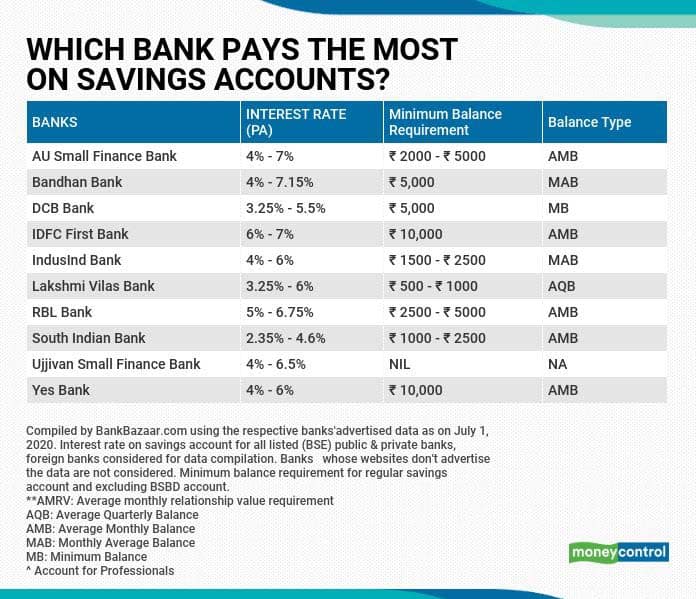

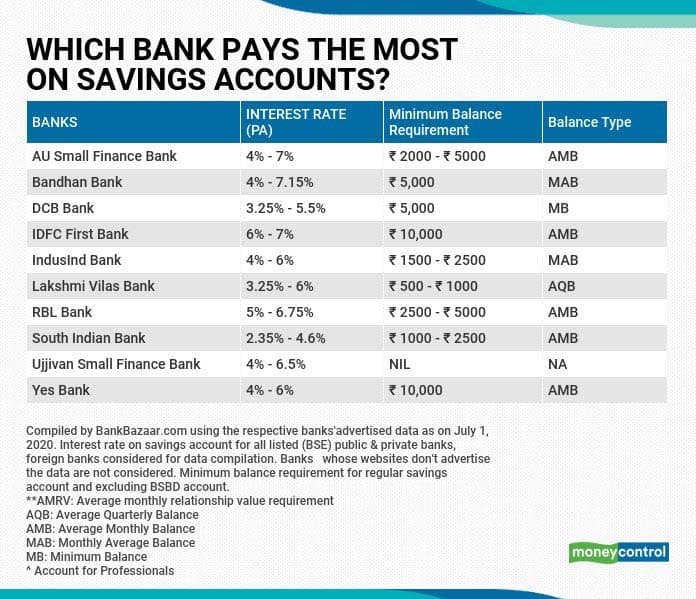

Finding the best savings account interest rate in India is no longer as simple as comparing one headline number. Many banks now use slab-based or progressive interest rates, where the return depends on your balance. For example, some private banks may offer lower rates on balances up to ₹3 lakh, higher rates on balances above ₹3 lakh, and different rates again for very large deposits. This makes it important to compare not just the advertised rate, but also the balance range, payout frequency, safety, charges, and account features.

What Is a Good Savings Account Interest Rate in India?

A good savings account interest rate in India typically depends on the type of bank. Large public sector banks usually offer lower savings rates, while private banks and small finance banks may offer higher rates to attract deposits. Many leading banks offer around 2.50% to 3.50% p.a. on basic balances, while select banks may offer 5% to 7% p.a. or more on higher slabs.

However, the highest rate is not always the best choice. You should check whether the rate applies to your full balance or only to the incremental amount above a certain threshold. You should also consider minimum balance rules, digital banking quality, branch access, debit card fees, and deposit insurance coverage.

Comparison: Best Savings Account Interest Rates in India

| Bank Type / Example | Indicative Savings Interest Rate | Best For | Key Point to Check |

|---|---|---|---|

| Large PSU Bank such as SBI | Usually around 2.70% to 3.00% p.a. | Safety, branch access, salary accounts | Rates are stable but generally lower |

| Private Bank such as Axis Bank | Often around 3.00% to 3.50% p.a. | Digital banking and service network | Check balance slabs and service charges |

| Private Bank with High Slab Rates | Can be around 5.00% to 7.00% p.a. on select slabs | Emergency funds of ₹5 lakh to ₹25 lakh | Understand progressive slab calculation |

| Small Finance Banks | May offer higher rates on specific balance ranges | Rate-focused savers | Check RBI regulation, DICGC cover, and liquidity |

How Progressive Savings Account Interest Slabs Work

Many people searching for the best savings account interest rate India miss one important detail: progressive slabs. Suppose a bank offers 2.50% p.a. up to ₹3 lakh, 6.50% p.a. above ₹3 lakh up to ₹25 crore, and 5.00% p.a. above ₹25 crore. This does not always mean your entire balance earns 6.50%. In a progressive structure, different portions of your balance may earn different rates.

For example, if you keep ₹7 lakh, the first ₹3 lakh may earn 2.50%, while the amount above ₹3 lakh may earn the higher slab rate. This is why your effective yield may be lower than the headline rate. Always read the bank’s interest calculation method before opening the account.

Best Savings Account Interest Rate India: SBI and Government Banks

Savings Account Interest Rate SBI

SBI is one of India’s most trusted banks, but it usually does not offer the highest savings account interest rate. SBI savings account rates are generally in the lower range compared with private banks and small finance banks. The main advantages are trust, large branch network, ATM access, government-linked services, and convenience for pensions, subsidies, and salary credits.

Which Government Bank Gives the Highest Interest Rate on Savings Account?

Among government banks, rates are often similar and usually lower than aggressive private-sector or small finance bank offers. Some public sector banks may occasionally offer slightly better rates on certain balances, but the difference is generally modest. If your priority is the highest return, private banks or small finance banks may be more competitive. If your priority is government-bank comfort, compare SBI, Bank of Baroda, Canara Bank, Punjab National Bank, Indian Bank, and Union Bank using their latest published rate cards.

Which Bank Gives Monthly Interest on Savings Account?

Most banks calculate savings account interest on the daily closing balance, but the crediting frequency can vary. Many banks credit interest quarterly, while some may offer monthly interest credit on savings accounts. Monthly interest credit can be useful for retirees, freelancers, and households that want regular cash flow. However, do not select an account only because it credits monthly interest. A quarterly-crediting account with a higher effective rate may still be better.

Best Savings Account for Senior Citizens in India

Senior citizens often look for a higher savings account interest rate, but banks usually provide special senior-citizen rates on fixed deposits, not regular savings accounts. For liquidity, seniors can keep 3 to 6 months of expenses in a high-interest savings account and move surplus funds to senior citizen fixed deposits, the Senior Citizens’ Savings Scheme, or short-duration debt products depending on risk profile.

Interest from savings accounts is taxable. Non-senior citizens can claim deduction up to ₹10,000 under Section 80TTA on savings interest. Senior citizens can claim a higher deduction under Section 80TTB, up to ₹50,000, covering interest from savings and deposits. Tax rules may change, so consult a tax professional for large balances.

How to Choose the Best Savings Account Interest Rate in India

1. Match the Rate with Your Balance

If you plan to keep only ₹50,000 to ₹2 lakh, a bank offering high rates only above ₹5 lakh may not help. If you maintain ₹6 lakh to ₹10 lakh as an emergency fund, slab-based high-interest accounts can be attractive.

2. Check Minimum Balance and Charges

High interest can be offset by debit card fees, non-maintenance charges, cash transaction fees, and SMS charges. Always compare the total cost.

3. Prioritise Safety and Liquidity

Bank deposits are covered by DICGC insurance up to ₹5 lakh per depositor per bank, including principal and interest. For very large balances, consider spreading money across multiple banks.

4. Track Your Interest and Cash Flow

Use a simple budget planner, calculator, or personal finance notebook to track balances, interest credits, and tax liability. A good financial calculator or household budgeting tool can help you compare effective returns before switching banks [AMAZON_LINK].

Final Verdict

The best savings account interest rate in India depends on your balance and usage. SBI and government banks are strong for trust and accessibility, but they may not offer the highest rates. Private banks and small finance banks can offer better returns, especially on higher slabs, but you must review the fine print. For emergency funds, choose a bank that combines a competitive rate, easy withdrawals, low charges, strong digital access, and reliable customer service.

FAQ

1. Which bank gives the best savings account interest rate in India?

Private banks and small finance banks often offer the highest savings account rates on specific balance slabs. The best bank depends on your average balance and whether the rate applies progressively.

2. What is the SBI savings account interest rate?

SBI savings account rates are generally lower than many private and small finance banks, often around the 2.70% to 3.00% p.a. range. Check SBI’s official website for the latest rate.

3. Do senior citizens get higher savings account interest?

Usually, senior citizens get higher rates on fixed deposits, not savings accounts. However, they may receive better tax deductions on interest income under Section 80TTB.

4. Which bank gives monthly interest on a savings account?

Some banks offer monthly interest credit, while many credit interest quarterly. Always confirm the payout frequency and compare the effective return.

5. Is it safe to keep ₹10 lakh or more in a savings account?

It is liquid and convenient, but DICGC insurance covers only up to ₹5 lakh per depositor per bank. For larger balances, spreading funds across banks may reduce risk.